Weekly Alpha #58: Why I’m Paying Attention to Venice AI and VVV

Venice has gone from an interesting privacy-AI product to something I’m actually using more, and VVV’s tokenomics are starting to reflect that shift.

Hello everyone,

Bitcoin is consolidating, but the market is not quiet.

Some of the strongest moves are happening away from the majors, in names tied to clear narratives. One of the clearest for me right now is VVV, the token behind Venice AI.

I do not think this is just another AI ticker moving because the sector is hot. What makes Venice interesting is that the product has started to matter more to me personally, and the tokenomics are moving in a direction that is worth paying attention to.

Venice: Private AI With a Product Behind It

The reason Venice caught my attention is simple: people want AI tools, but they do not necessarily want to hand over all their data to use them.

I’ve been using AI a lot, whether it is Cursor, Codex, Claude, or other tools for research and my work as a developer. The more I use them, the more obvious the privacy tradeoff becomes.

These tools are useful, but I still catch myself thinking twice before pasting in research notes, wallet activity, strategy ideas, or client work.

Local models are getting better, and I like the direction. But right now, they still do not feel as strong as the best hosted models for many workflows. That is where Venice becomes interesting: it tries to give users access to strong AI models without making them hand over everything in the process.

I had tried Venice before, but for a while it did not really stick in my workflow. It was interesting, but not good enough to replace the tools I was already using.

That has started to change. Over time, I’ve found myself using it more naturally, not because I forced myself to, but because the product has improved enough to earn more of my attention.

The founder matters too. Venice was started by Erik Voorhees, someone I’ve followed in crypto for a long time. He has been around since the early Bitcoin days, and I tend to pay attention when builders with that kind of history are working on something new.

That does not remove the risk, of course. Founder reputation is not a thesis by itself. But in a space full of thin AI wrappers and short-lived narratives, it does make Venice more interesting to me.

None of this automatically makes VVV a winner, but it does make the narrative easier to understand.

Tokenomics: What Actually Matters

The interesting part about VVV is not just that it is an AI token. There are plenty of those.

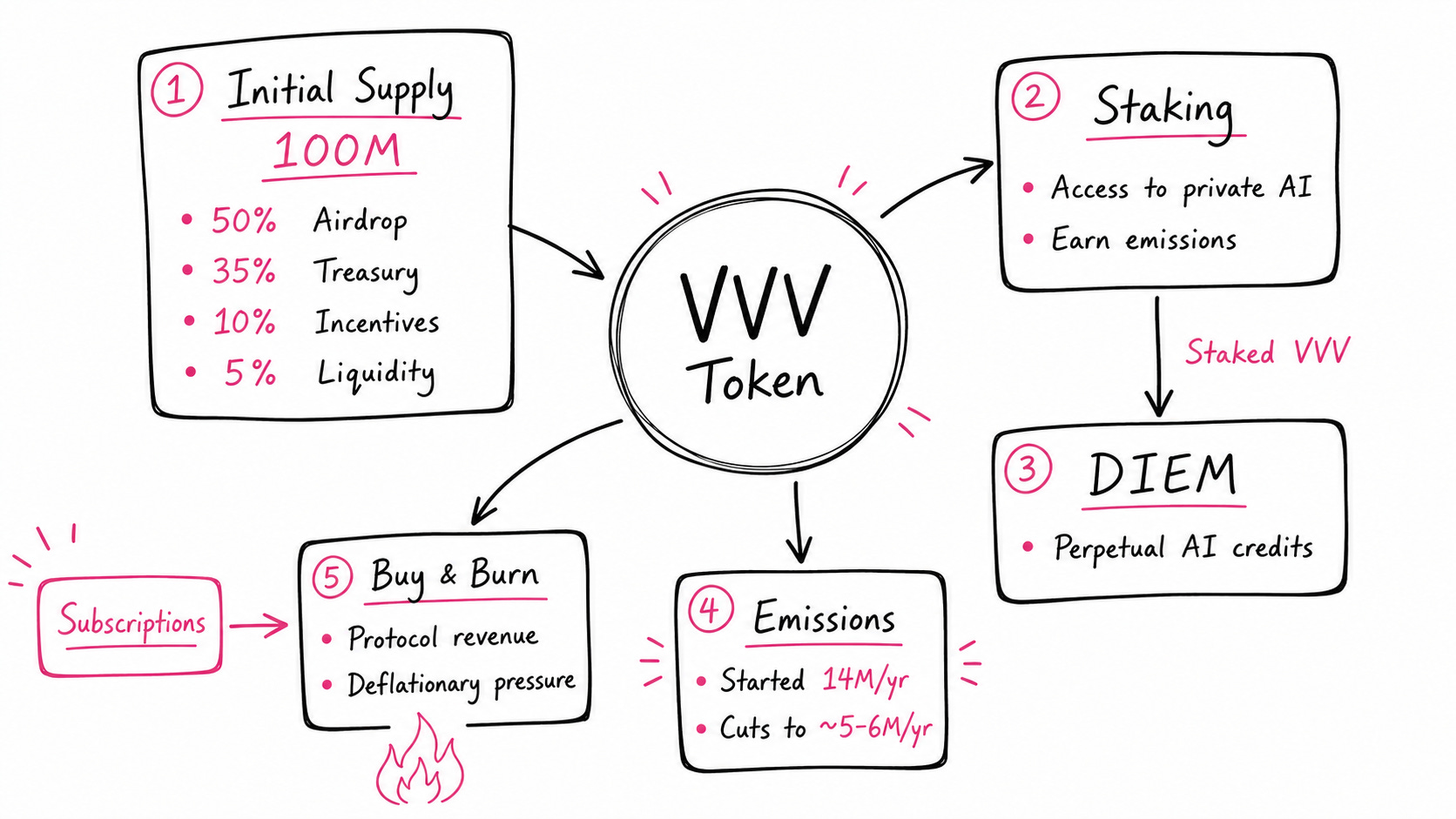

The more important part is how quickly the tokenomics have changed. Venice started with a fairly standard setup: a 100M genesis supply, a large airdrop, and high emissions for stakers.

The Supply Reset

Since launch, the direction has been clear: less loose supply, lower emissions, more staking, and a stronger link between VVV and actual Venice usage.

VVV launched with a 100M supply, and 50M VVV, or 50%, was allocated to the airdrop. The claim window lasted 45 days and included Venice users, AERO holders, and several AI-related communities.

There was one allocation issue: vAERO holders were excluded. I was one of them. I asked Erik Voorhees about it on X, and he told me it was a mistake. Annoying for me, but the more important part came after the claim window closed.

By the end of the window, around 17.4M VVV had been claimed by more than 40k wallets. That left roughly 32.6M VVV unclaimed, about 65% of the airdrop allocation and close to one-third of the original supply.

Instead of leaving those tokens sitting in the treasury, Venice burned them in one event.

That matters because airdropped tokens often struggle with loose supply and constant sell pressure. Burning the unclaimed allocation did not magically create demand, but it did remove a meaningful overhang early in the token’s life.

Venice also sold 1M VVV from the team’s unlocked allocation on launch day, then bought it back and burned it after community pushback. That shows the team was responsive, but it also reminds you that execution risk is real.

The important point: VVV did not keep the full 100M launch supply floating around. A meaningful part of the original allocation was removed early, which made the supply side cleaner than it looked at launch.

Emissions cuts

Tokenomics matter a lot for this kind of project. The product can technically run without the token, but the token is what connects usage, staking, emissions, and supply. That makes the emission schedule worth paying attention to.

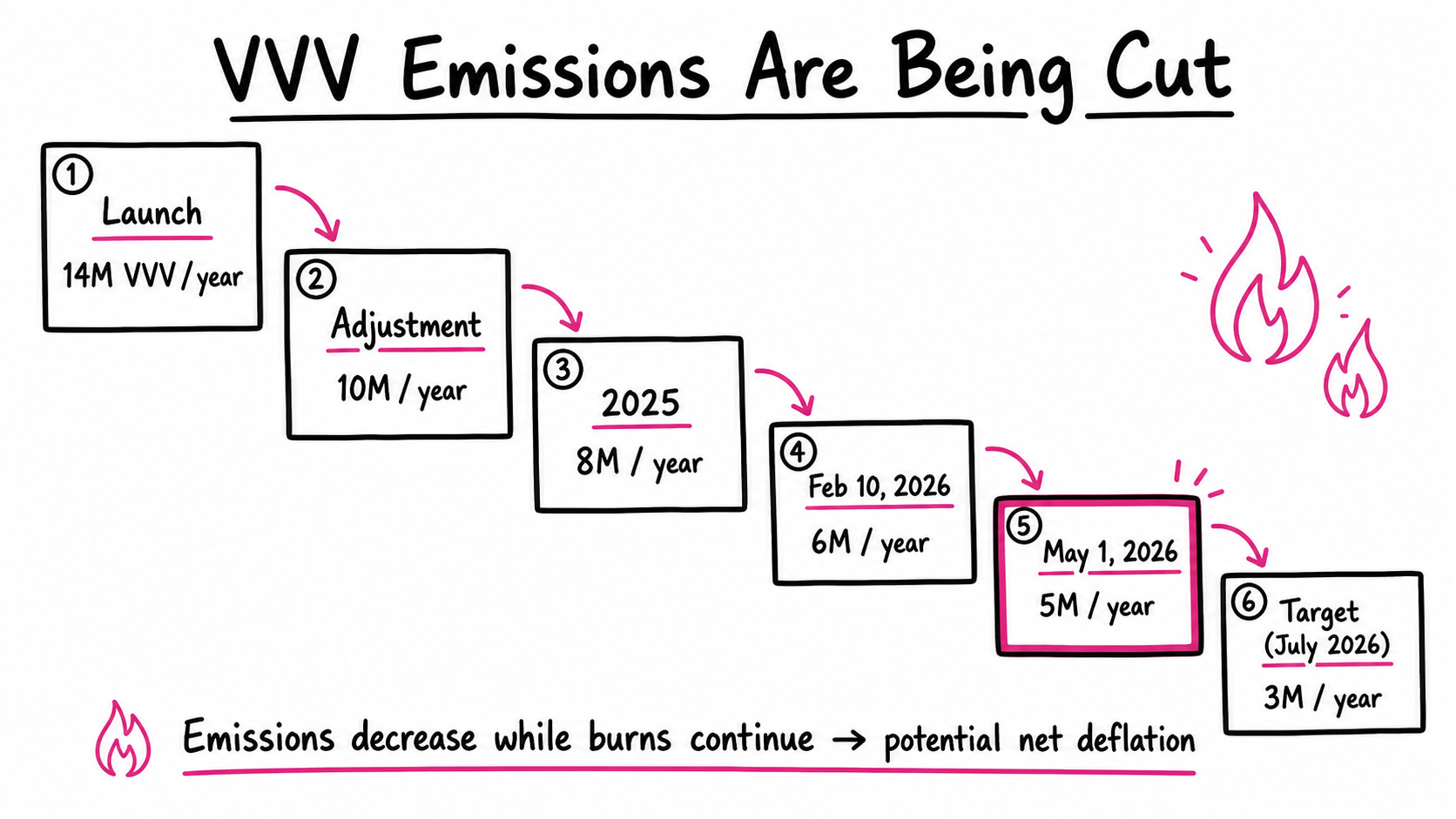

Venice has cut emissions four times in under a year, from 14M VVV annually down to 5M today, with 3M targeted by July 2026, a 79% reduction in roughly 18 months.

Less new supply hitting the market each month means less structural sell pressure, which is good for existing holders. The schedule is public and credible, which is why some early positioning has already happened.

But it’s still a speculative bet. Emission cuts reduce inflation but don’t guarantee price. VVV’s value over the next year depends on product adoption, trading volume, and how the broader market treats the sector. A token with falling supply but stagnating usage doesn’t pump. And right now it’s genuinely hard to know whether the current price already prices in the full cut schedule or not.

Having some exposure here is probably reasonable. Treating the emission schedule as a guaranteed price catalyst is not.

Staking: Why The Float Matters

The next important piece is staking.

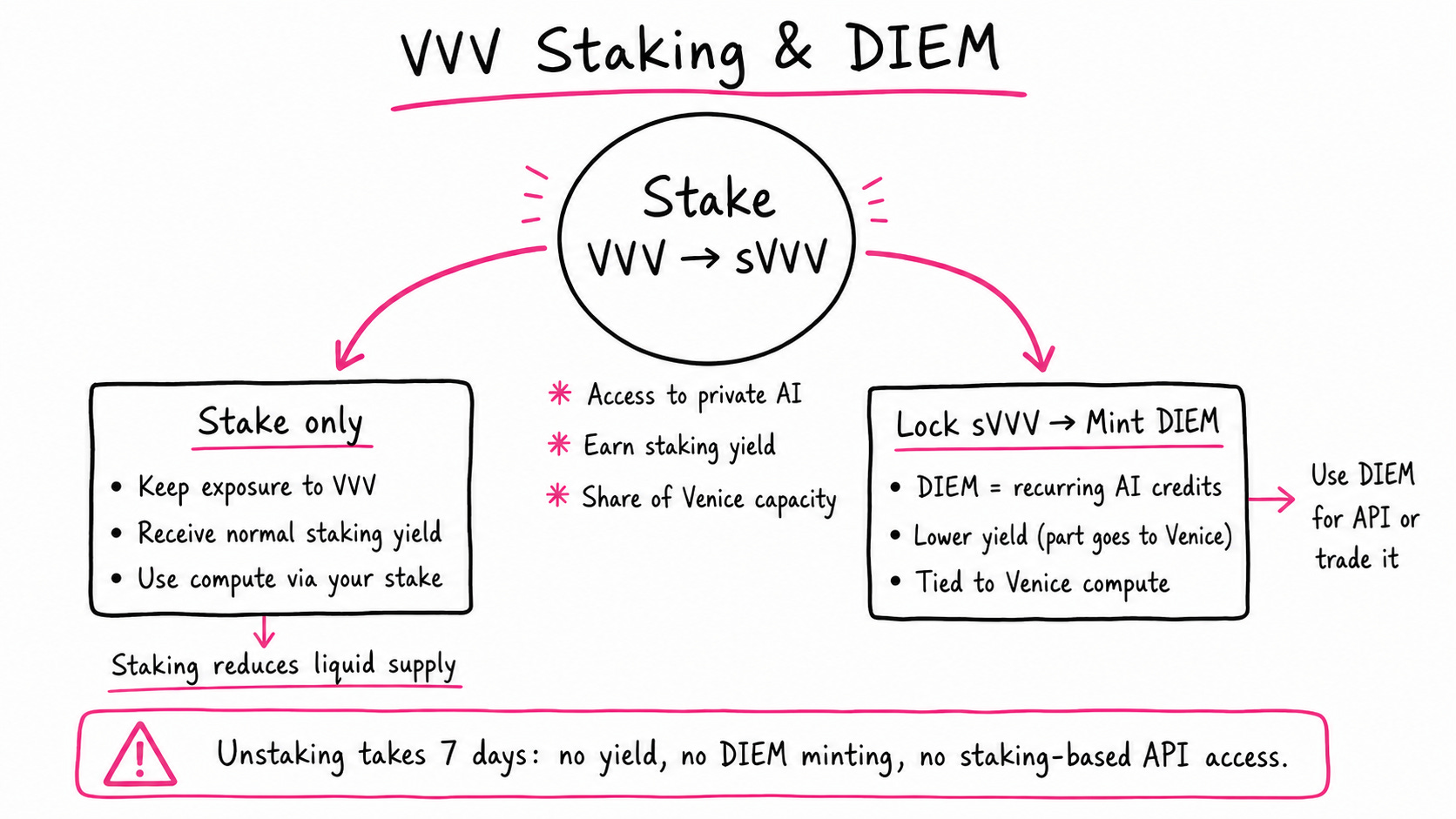

With VVV, staking is not just about earning yield. When you stake VVV, you receive sVVV, which gives you access to a share of Venice’s API capacity. So stakers are not only farming emissions. They are also reserving part of the network’s private AI compute.

That is where the model gets more interesting.

If you simply stake VVV, you keep exposure to the token, earn emissions, and get access to Venice compute through your staked position. At current parameters, the yield is around the mid-teens, although that can change over time.

DIEM adds another layer.

By locking sVVV, users can mint DIEM, a tokenized form of AI credit. Each DIEM represents ongoing API credit inside Venice. So VVV starts to look less like a normal speculative token and more like a capital asset: you lock it, and it gives you access to compute.

There is a tradeoff. If you mint DIEM, your sVVV is locked, and you receive a lower share of the normal staking yield. The rest goes back to Venice as compensation for providing the compute behind DIEM.

DIEM can then be used for API access or traded, which gives users a way to monetize compute without selling their original VVV.

The important point is that staking reduces liquid supply, but it also gives people a reason to hold the token beyond price speculation. Large stakers are not just betting on the chart. They are reserving a slice of Venice’s AI capacity.

There is still liquidity risk. Unstaking takes seven days, and during that period users do not earn yield, cannot mint DIEM, and lose staking-based API access. So staking creates real lock-in. That can be powerful when demand is rising, but painful if people want to exit quickly.

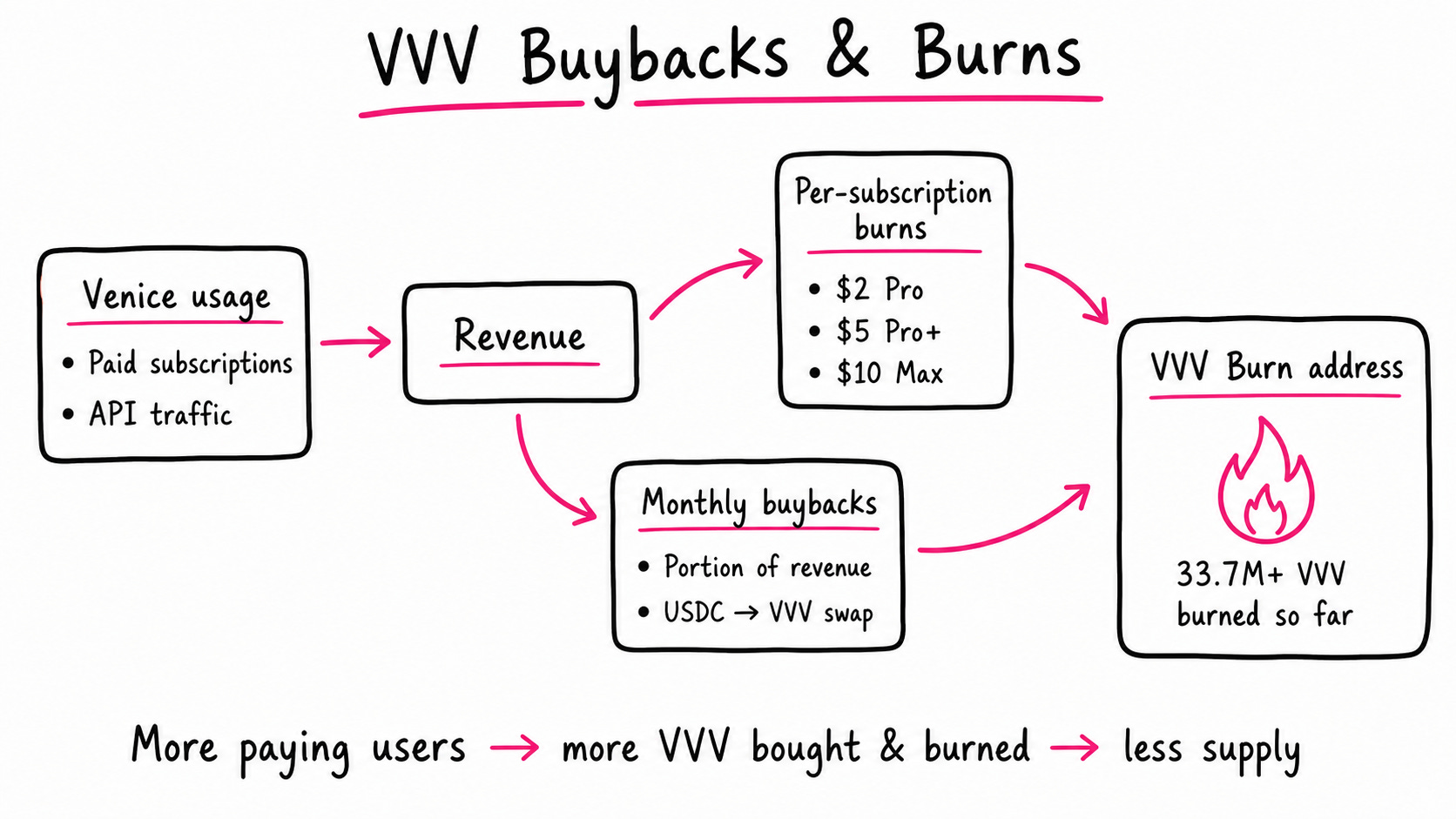

Buybacks & Burns: The Usage Link

The last piece is the buyback and burn mechanism.

This matters because it connects Venice usage back to VVV. If more people pay for Venice, part of that revenue can be used to buy VVV on the market and send those tokens to a burn address.

Venice started monthly revenue-funded burns in late 2025. The first one, in December, burned about 57k VVV using revenue from the previous month.

Then in April 2026, Venice added a more automatic version of the same idea. Every new paid subscription now triggers a VVV buyback and burn, with the amount depending on the plan: $2 for Pro, $5 for Pro+, and $10 for Max.

Those buys happen on-chain through USDC to VVV swaps, and the tokens are sent directly to the burn address. There is also a public burn tracker, so you can follow the transactions.

Put simply, more paying users means more revenue, more VVV bought from the market, and more VVV removed from supply.

A lot of tokens talk about usage, but the token itself never really captures it. With VVV, the mechanism is clearer. If Venice grows as a product, the burn program gives that growth a direct path back into the token.

So far, the numbers are already meaningful. Including the large airdrop burn and the revenue-funded burns, Venice reports that more than 33.7M VVV has been burned. Depending on whether you measure against genesis supply or adjusted circulating supply, that is roughly one-third of the original token supply and a much larger share of the current float.

That does not mean VVV only goes up. Burns are not magic. If demand falls, if emissions stay too high, or if the product stops growing, the token can still struggle.

But this is what you want to see: emissions coming down, supply being locked through staking, and real product revenue being used to remove tokens from circulation.

That is a cleaner setup than most AI tokens have.

Conclusion

Venice is one of my favorite projects to follow right now, which is why I wanted to spend time going through the mechanics instead of only talking about the narrative.

I like the founder. I like the team’s direction. More importantly, I like that the product is improving while the tokenomics are becoming more holder-friendly. That combination is rare enough to pay attention to.

My plan is simple: keep using Venice, keep tracking the numbers, and DCA over time if the thesis continues to hold.

The product itself matters here. When I first tried Venice, it felt interesting but still rough. The models were not good enough for me to use it regularly. That has changed. The experience is much better now, and I find myself using it more naturally, especially when privacy matters.

That is the bigger opportunity. Venice is not only a crypto product. It can also speak to people who care about private AI for work, research, personal use, or simply saying what they think without feeding everything into a closed system.

The bet is not just that AI stays hot. The bet is that private AI becomes useful enough for people to pay for it.

VVV is still a high-risk token, and nothing here is guaranteed. But if Venice keeps improving the product, growing revenue, reducing emissions, and burning supply, I think it has a real shot at becoming one of the stronger AI trades of the next cycle.

Onchain Analytics 🧐

This is where I share what I’ve actually been looking at onchain. The stuff that shapes how I’m positioning, not just what I’m buying.

Hyperliquid: Fees Keep Climbing

As you probably know, Hyperliquid has been on a strong run lately, with HYPE

recently pushing to a new all-time high. But the more important part is that the protocol is still generating a lot of fees, and those fees matter because they feed back into HYPE through the Assistance Fund.

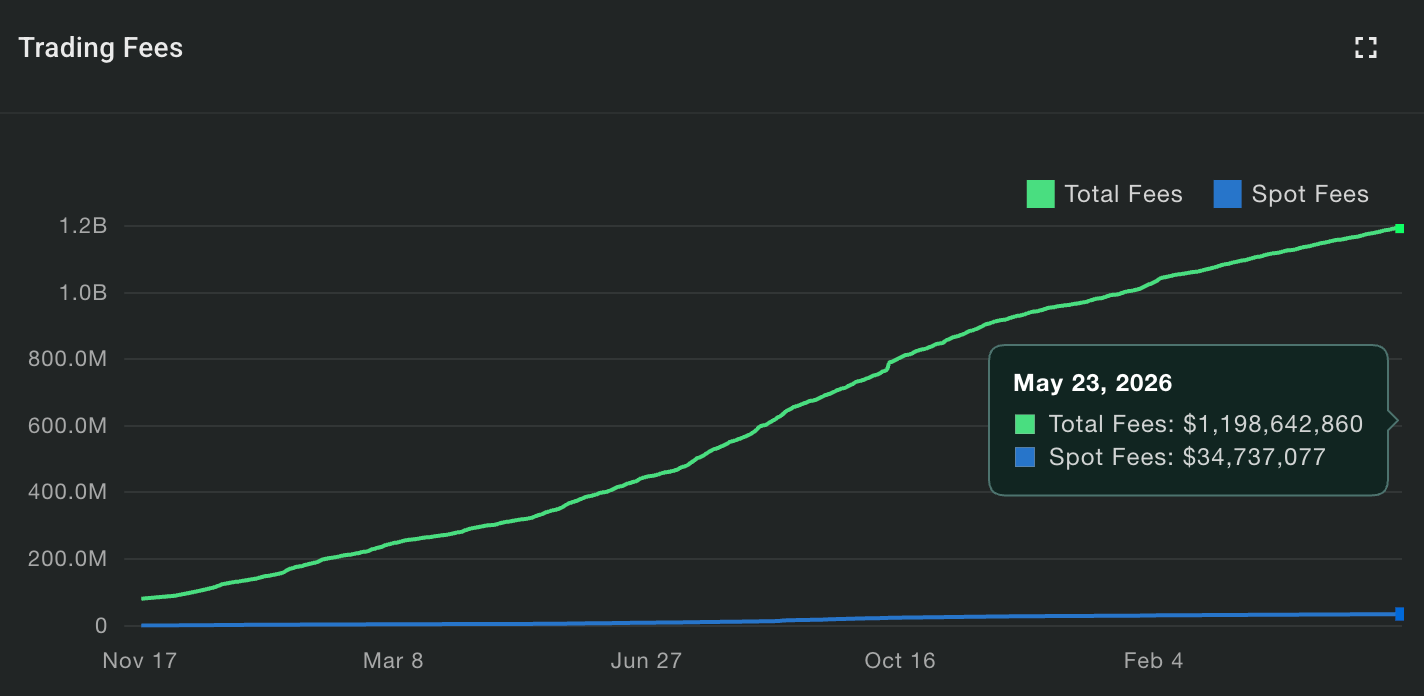

The first chart I’m watching is Hyperliquid trading fees.

According to HypurrScan, Hyperliquid has now generated roughly $1.2B in cumulative trading fees, with spot fees representing only around $35M of that total.

That tells you two things.

First, Hyperliquid is still mainly a perp machine. Spot exists, but the core business is still leveraged trading. Most of the fee growth is coming from traders using the perpetuals exchange, not from spot activity.

Second, the fee curve is still moving up. This is not a vanity metric like TVL that can sit still and look impressive. Fees require activity. Traders have to show up, place orders, take risk, and pay for execution.

That is why this chart matters. Even in a consolidating market, Hyperliquid continues to generate real trading fees at scale. For HYPE, that keeps the thesis alive: the network is not just attracting attention, it is producing measurable onchain activity.

The caveat is that this is cumulative data, so the line will almost always go up. What matters from here is the slope. If the curve keeps steepening, activity is accelerating. If it flattens, volume is slowing down.

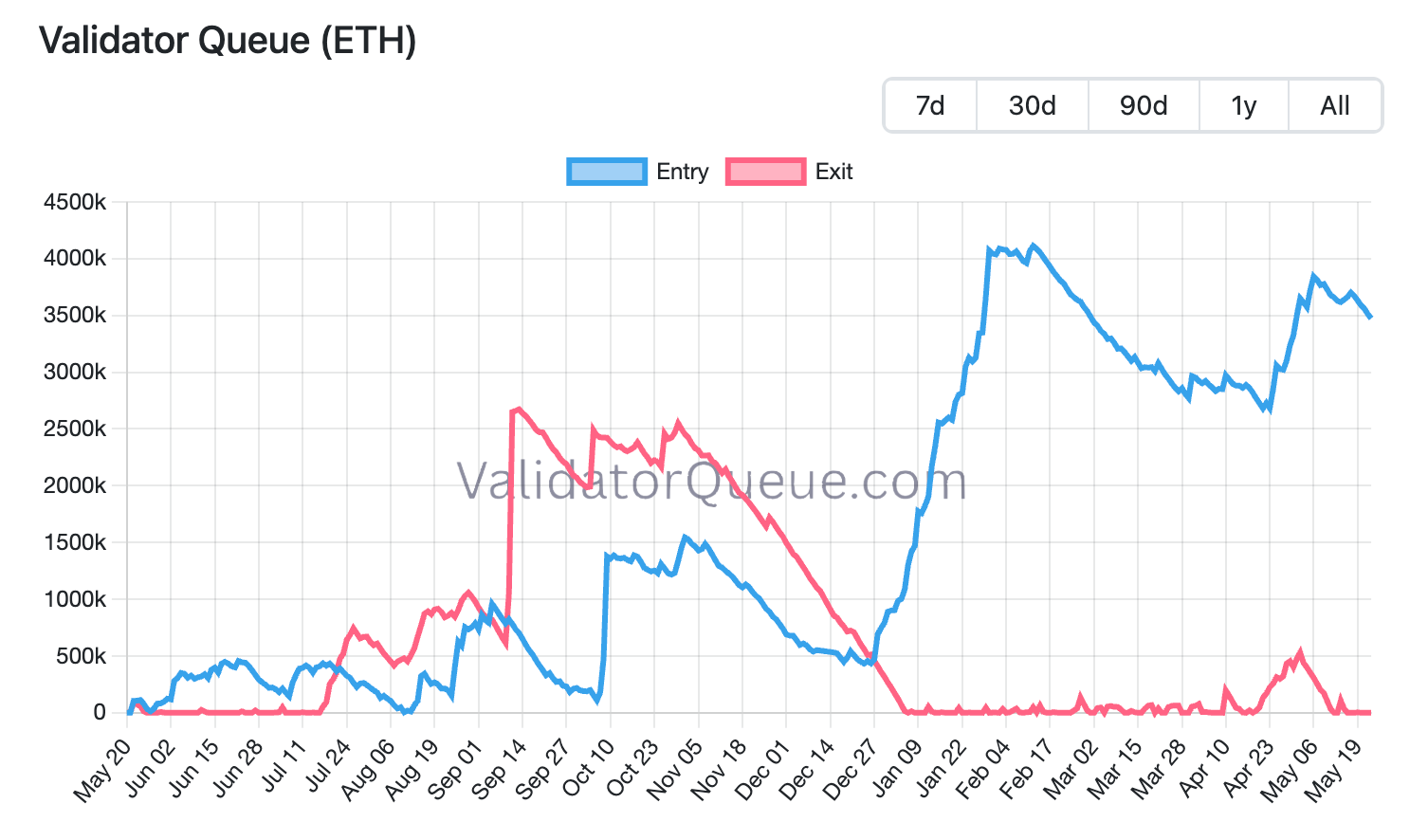

Ethereum: The Validator Queue Is Telling A Different Story

3.46M ETH is sitting in the validator entry queue. The exit queue is at zero.

That is not a trivial gap.

Validators are not trapped. The exit queue is empty, with only the sweep delay before funds clear after exit. So this is not a case where everyone wants out but cannot leave.

According to ValidatorQueue, the estimated wait to enter staking is around 60 days. That is a meaningful commitment. Anyone joining that queue anyway is making a deliberate long-term bet on Ethereum security, yield, and settlement demand. Not a reactive one.

The asset price is not reflecting this. ETH has been quiet while other things run. The market can ignore on-chain fundamentals for long stretches, and this is not an argument that price has to move immediately.

But it does push back against the “Ethereum is dead” read. Dead protocols do not usually have 60-day validator wait lists with empty exits.

The chart worth tracking is simple: if the entry queue stays elevated and exits stay near zero, this signal holds. If entries start draining and exits pick up, the read changes. Until then, the queue is telling a different story than the price.

This Week’s Intel 📚

Here’s what was actually worth reading this week.

Bitcoin Billionaire Books First SpaceX Mars Mission - read

Kalshi, Polymarket lose bids to halt Nevada and Washington gambling cases - read

NEAR token jumps 30% amid AI hype, Arthur Hayes endorsement and scaling plans - read

DeFi hacks shake institutional confidence as risks outpace yields - read

Polymarket Hit By ‘Internal Top-Up’ Wallet Exploit, $700K Drained - read

Ethereum is still a good long-term buy, according data: Analyst - read

Podcast Picks 🎧

Podcasts worth your time this week.

That’s it for this week.

If you found this useful, share it with someone who is trying to make sense of this market.

You can also follow me on X and Farcaster for more frequent updates.

Nothing in this newsletter is financial advice.

I personally use many of the protocols I write about, but that does not make them safe. Crypto is risky, DeFi is risky, and things can break quickly.

Do your own research, size positions carefully, and never invest more than you can afford to lose.