Weekly Alpha #60: Pendle's Quiet Breakout Week

Pendle held up during the crash. The reason might matter more than the price action.

In this edition of The Weekly Alpha:

🧑🌾 Pendle's Quiet Breakout Week

🧐 Onchain Analytics

📚 This Week's Intel

🎧 Podcast Picks

Hello everyone,

Crypto had a rough week.

BTC briefly traded below $60K, ETH was down more than 20% on the week, and roughly $1.6B in leverage was wiped out in a single day. CoinDesk framed it as the worst weekly drop for BTC and ETH since the FTX collapse, which gives you an idea of how violent the move felt.

But not everything traded the same.

Pendle was down too, but it held up better than most DeFi tokens. While ETH and AAVE were down more than 20%, PENDLE was down closer to 9% depending on the snapshot you use.

That alone does not make it a buy. Small caps can move strangely during crashes. But the timing was interesting.

During the same week, Pendle got two important catalysts: Revolut listed PENDLE for European users, and Sky, the protocol formerly known as MakerDAO, launched fixed-rate yield through Pendle.

That is the story this week.

Not just that PENDLE outperformed. More that the market had a stress event, and Pendle’s core product suddenly looked more useful.

Pendle’s Quiet Breakout Week

Let me start with the simple version.

Pendle is a yield tokenization protocol. It lets users split yield-bearing assets into two parts: the principal and the future yield.

That sounds boring until markets start breaking.

In a calm market, fixed-rate yield can feel like a niche product. In a crash week, it starts to make more sense. Some users want upside from variable rates, especially when borrow demand spikes. Others just want to lock a fixed return and stop thinking about it.

Pendle sits directly in that trade.

Revolut listed PENDLE

The Revolut listing matters because it changes distribution.

A lot of crypto-native listings are just more access for people who were already going to buy the token anyway. Revolut is different. It puts PENDLE inside an app that many retail users already treat like a bank account.

I would not overstate it. A listing is not product-market fit by itself.

But for a protocol like Pendle, distribution matters. Yield tokenization is still hard to explain to normal users. If a major fintech app starts giving the token more visibility, the top of the funnel gets a lot wider.

Sky launched fixed-rate yield through Pendle

This is the stronger catalyst in my opinion.

Sky, the protocol behind USDS and sUSDS, launched fixed-rate yield using Pendle’s infrastructure. The fixed-rate product was around 42%, and it is tied to one of the largest stablecoin pools in DeFi.

That matters because Pendle is not only serving degen yield chasers here. It is being used by a large stablecoin protocol to package yield in a cleaner way.

This is the kind of integration that makes the thesis easier to understand.

Pendle is not just a place to speculate on APY. It can become infrastructure for treasuries, stablecoin protocols, and users who want predictable returns in DeFi.

Why volatility helps the Pendle story

This week was a good reminder that yield behaves differently in stress.

When markets crash, borrow demand can spike. Liquidations hit. Rates move around. Protocols like Aave and Morpho start printing fees because the lending engine is working harder.

Pendle is interesting because it lets users choose which side of that volatility they want.

YT holders can benefit when variable yield spikes. PT holders get the fixed-rate side and do not need to care as much about the daily rate chaos.

That is the product-market fit.

Not in a perfect bull market where everything goes up. In the messy weeks where people actually need to manage risk.

The PT-sUSDE pool on Pendle’s Plasma chain also matured this week, with roughly $190M in fixed-rate yield paying out as expected. That kind of reliability is exactly what treasury managers and larger allocators care about.

Ticker: PENDLE, around $1.20 at the time of writing. Market cap around $200M, FDV around $340M.

The other side

There are real risks.

PENDLE is still down massively from its 2024 high. The token does not have a hard max supply, so emissions matter. TVL also fell this week, even if part of that was just asset prices dropping.

And at this market cap, PENDLE is still small by DeFi standards. One large seller can move the chart.

So I would not frame this as a clean breakout yet.

The better framing is this: Pendle had a real stress test, held up better than most DeFi tokens, and picked up two integrations that strengthen the long-term yield tokenization thesis.

That is worth paying attention to.

Onchain Analytics 🧐

This is what stood out to me onchain this week.

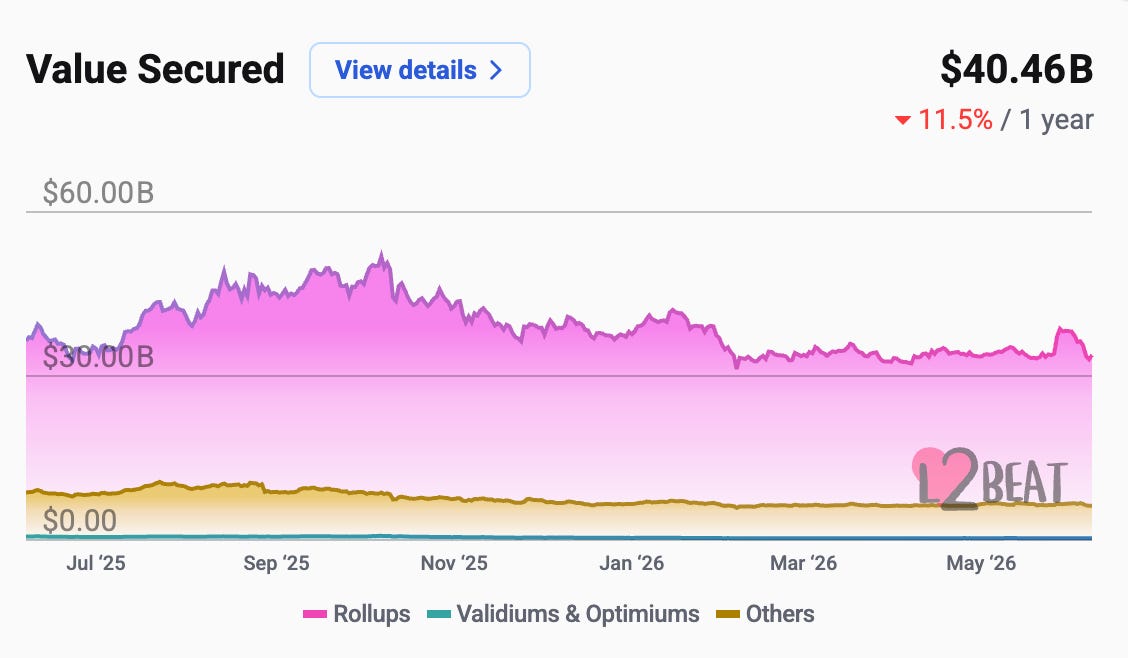

L2 TVL looked worse in dollars than it did in ETH

A lot of L2 dashboards looked ugly this week because ETH was down hard.

In USD terms, TVL dropped across most of the market. But that does not always mean capital left the ecosystem. Sometimes it just means the asset used to measure the ecosystem got repriced.

That is why I like checking both USD and native asset terms during weeks like this.

The cleaner signal is that some L2s still showed deposit strength even while the dollar value fell. World Chain was one of the standouts, with strong TVS growth while most major L2s were red.

The caveat is important: World Chain is still Stage 0, so the security model is not where I would want it to be for large long-term allocations.

But the inflows are still worth watching.

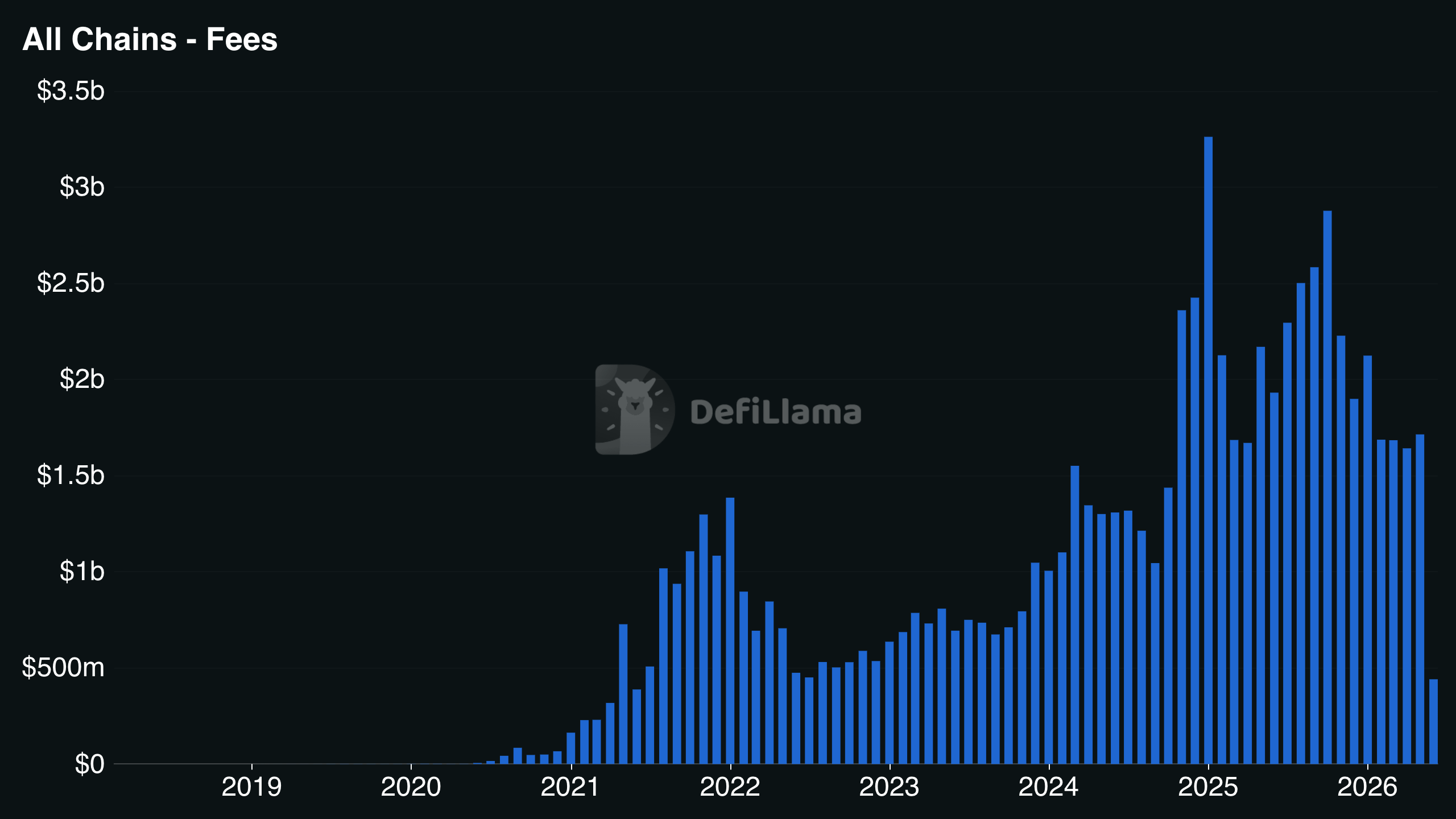

Fees showed where the stress went

The biggest fee spikes this week were not only in the obvious places.

Aave V3 had a huge fee day as liquidations picked up. Morpho and Spark also benefited from the lending layer running hot.

That is not the same as organic growth.

It is a volatility fee spike. Useful signal, but not something I would treat as a clean growth trend by itself.

The more interesting part is that DeFi kept functioning. The lending protocols did what they were supposed to do during a rough deleveraging event.

Block builders also had a strong week. That makes sense. When liquidations, arbitrage, and volatility increase, MEV capture increases too.

It is a reminder that Ethereum’s fee economy is much bigger than just the apps we usually talk about.

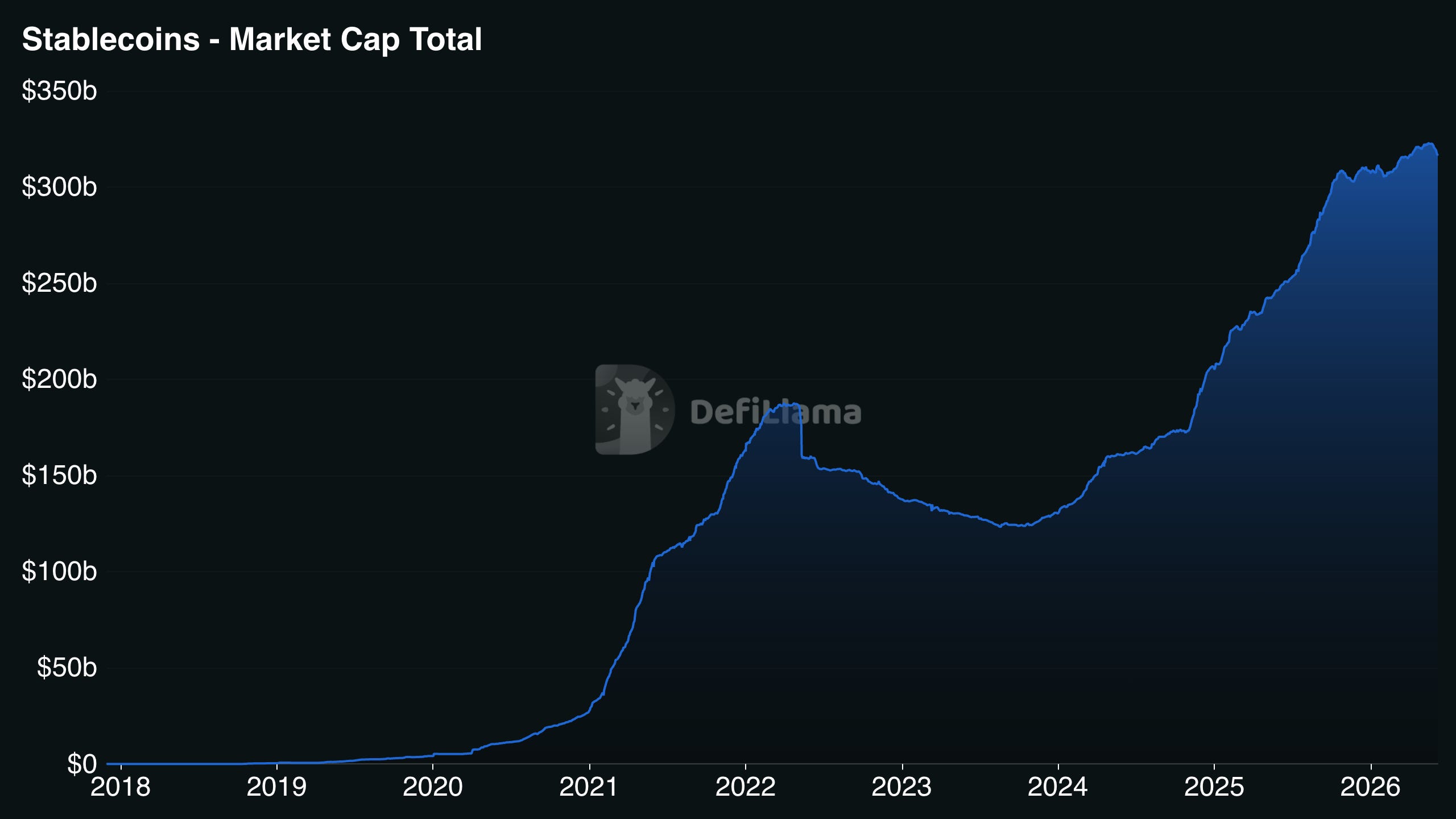

Stablecoins held up well

Stablecoin supply stayed around the $314B to $317B range depending on the source snapshot.

USDT is still around $187B. USDC is around $75B.

No major panic redemption signal there.

The one thing I am watching is Ethena’s USDe, which fell to around $4.5B. That makes sense if funding rates are shifting and delta-neutral strategies are being reduced.

For DeFi health, USDC staying steady is probably the cleaner signal

.

Hyperliquid is still a stress-test name

Hyperliquid’s TVS looked weak in dollar terms, but the more important question is whether deposits and trading activity hold up.

The perp venue still generated strong fees during the crash week. That is what you want to see from an exchange-like protocol during volatility.

The risk is still the same: HYPE and Hyperliquid are now a huge narrative, and huge narratives can unwind quickly when positioning gets crowded.

But from a usage perspective, it is still one of the more important protocols to track.

This Week’s Intel 📚

1. Zcash patched a critical Orchard vulnerability

Zcash disclosed and patched a serious Orchard vulnerability that could have allowed counterfeit ZEC creation inside the shielded pool.

That is the kind of bug that hits trust directly, especially for a privacy coin.

The important nuance is that Zcash Foundation said there was no evidence of an exploit. But the market still reacted hard because with shielded systems, proving what did or did not happen is harder than with a transparent ledger.

This is probably the most important privacy story of the week.

2. DeFi governance risk is becoming harder to ignore

Governance attacks and governance-related exploits keep showing up as a risk theme in 2026.

The problem is simple: a lot of protocols still have low voter participation, large idle treasuries, and governance systems that were not built for adversarial markets.

Flash-loan voting is only one version of the problem. Delegation, quorum design, timelocks, multisig control, and cross-chain governance all matter now.

This is worth tracking because the next major DeFi exploit may not be a smart contract bug. It may be a governance failure.

3. RWAs held up better than retail DeFi

The RWA sector still looks more resilient than the retail side of DeFi.

That fits the broader market structure story. Retail DeFi bleeds when leverage unwinds. Institutional RWA flows are usually slower, stickier, and less narrative-driven.

Pendle’s link with Sky and its Mu Digital integration in Asian credit markets fit into this trend.

This is also why I keep coming back to the same point: the next cycle probably will not be driven only by memecoins. RWAs, stablecoins, credit, yield, and settlement are still where the more durable onchain economy is forming.

4. Lighter is still getting attention

Lighter continues to show up in the perps conversation.

The Hyperliquid alternative thesis is easy to understand: high-performance perps, Ethereum L2 angle, zk verification, and a much earlier stage profile.

But it is still early.

Stage 0 on L2Beat means trust assumptions are still high. The product can be interesting while the infrastructure risk remains real.

That is exactly why I would track it, but not treat it like a proven Hyperliquid replacement yet.

5. World Chain had a strong week

World Chain was one of the few L2s showing clear strength during the drawdown.

The growth is worth watching because it happened during a week where most dashboards looked terrible.

The caveat is the same as above: Stage 0. Strong inflows do not remove the security question.

Podcast Picks 🎧

Bell Curve: What Brings Capital Back to DeFi?

This one fits the week well.

The main question is what actually brings capital back to DeFi after a market flush. Not just better charts, but better products, clearer yield, and protocols that can survive stress.

Empire: Hyperliquid Just Had Its Breakout Moment

A good short segment on Hyperliquid’s fee dominance and why HYPE is changing how people think about perp DEXs.

Useful if you want to understand why the market keeps treating Hyperliquid like more than just another exchange token.

That’s it for this week.

If you found this useful, share it with someone who is trying to make sense of this market.

You can also follow me on X and Farcaster for more frequent updates.

Nothing in this newsletter is financial advice.

I personally use many of the protocols I write about, but that does not make them safe. Crypto is risky, DeFi is risky, and things can break quickly.

Do your own research, size positions carefully, and never invest more than you can afford to lose.

The Sky/Pendle integration is the piece that changes the long-term thesis. When a protocol that manages one of the largest stablecoin pools in DeFi starts packaging yield through Pendle, it shifts Pendle from "degen yield speculation tool" to "DeFi yield infrastructure." That's a different product category with a different buyer profile.

The Revolut listing is interesting distribution, but you're right that listings alone don't create product-market fit. What makes this week different is that Pendle's core product — the PT/YT split — had a genuine use case during a stress event, not just in a calm bull market. Fixed-rate yield at 42% with predictable settlement hit differently when the rest of DeFi was deleveraging. The $190M PT-sUSDE maturity paying out cleanly during a crash is exactly the kind of evidence that moves institutional allocators from "aware of" to "interested in."