In this edition of The Weekly Alpha:

🧑🌾 5 Yield Opportunities on Base

🧐 Onchain Analytics

📚 This Week’s Intel

🎧 Podcast Picks

Base is not the loudest chain in crypto.

There is no Base token to trade. No airdrop campaign to farm. No governance chart for people to argue about every week.

That makes the chain easier to underrate.

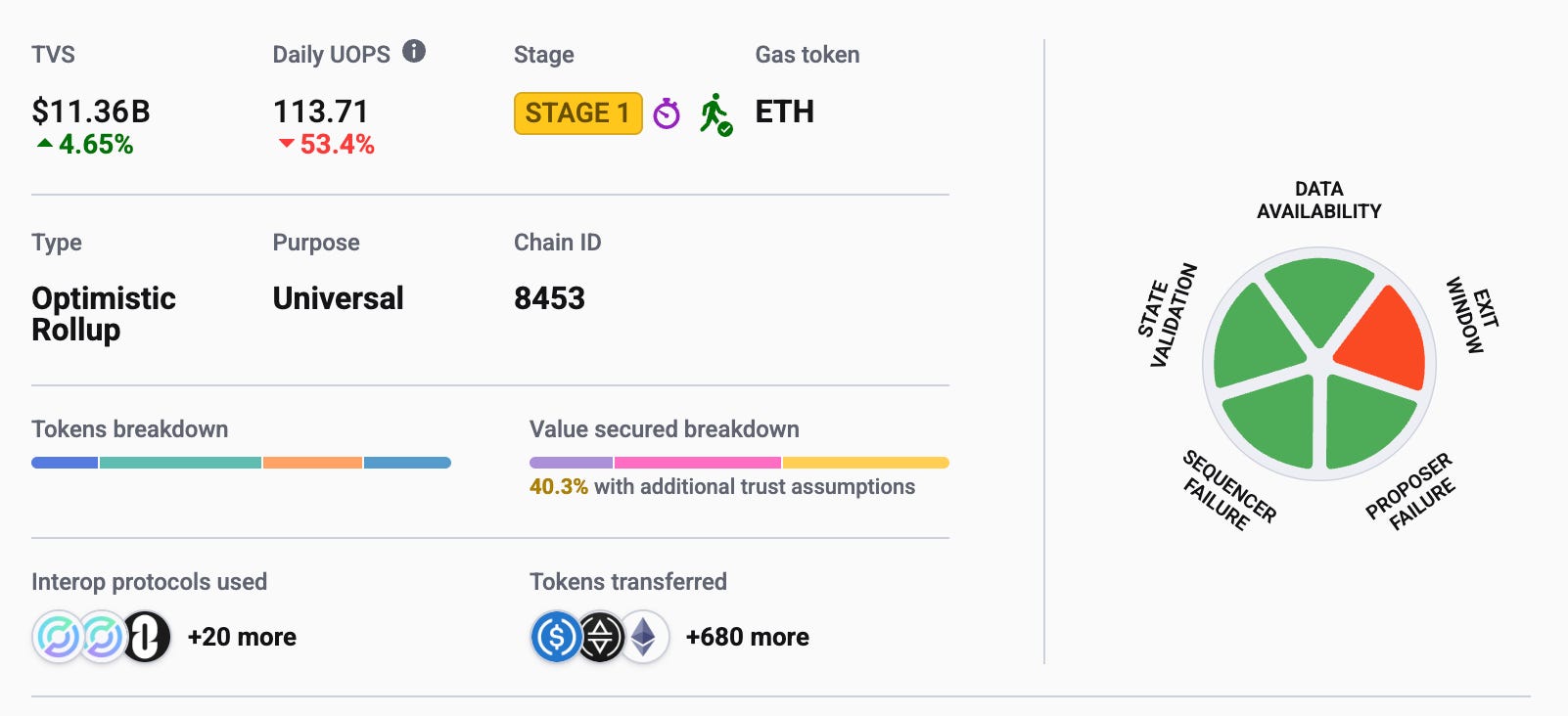

But the underlying numbers are getting harder to ignore. L2Beat has Base at roughly $11.35B in total value secured and Stage 1 today. DefiLlama shows about $4.0B in DeFi TVL, $4.8B in stablecoins, and around $7.7B in 7-day DEX volume on the chain.

That is the more interesting version of the Base story. It is not growing because people are chasing a native token. It is growing because Coinbase distribution, low fees, deep USDC liquidity, and a few strong native protocols are starting to create a real DeFi surface.

The practical question is simple: if Base is becoming one of the main places onchain capital sits, where is the yield?

Here are five Base yield opportunities I would look at first. APYs move quickly, so treat the numbers as a dashboard snapshot, not a promise.

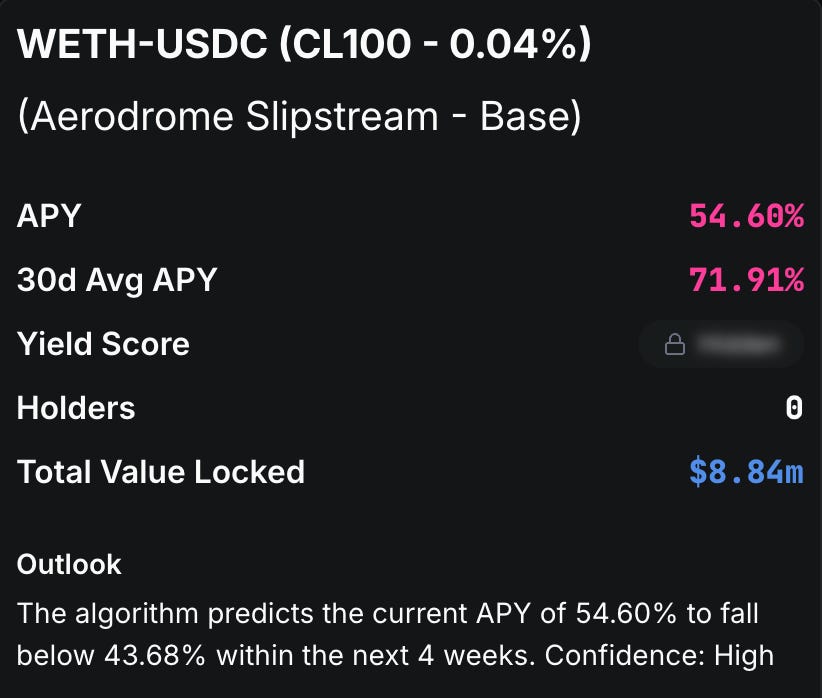

1. Aerodrome Slipstream WETH/USDC

Aerodrome is still the main native DEX on Base.

Its WETH/USDC Slipstream pool is the highest-yield option on this list, with the current dashboard snapshot showing roughly 54% APY. That comes from two places: swap fees and AERO emissions.

This is not passive yield. It is concentrated liquidity. You choose a range, collect fees when trades pass through it, and take impermanent loss if price moves hard enough against your position.

That tradeoff is fine if you know what you are doing. It is not fine if you look at the APY and assume it behaves like a lending vault.

The real signal is that Aerodrome continues to matter for Base liquidity. If Base activity keeps growing, Aerodrome remains one of the cleanest ways to express that view. Just remember that part of the yield depends on AERO incentives, and incentives can move.

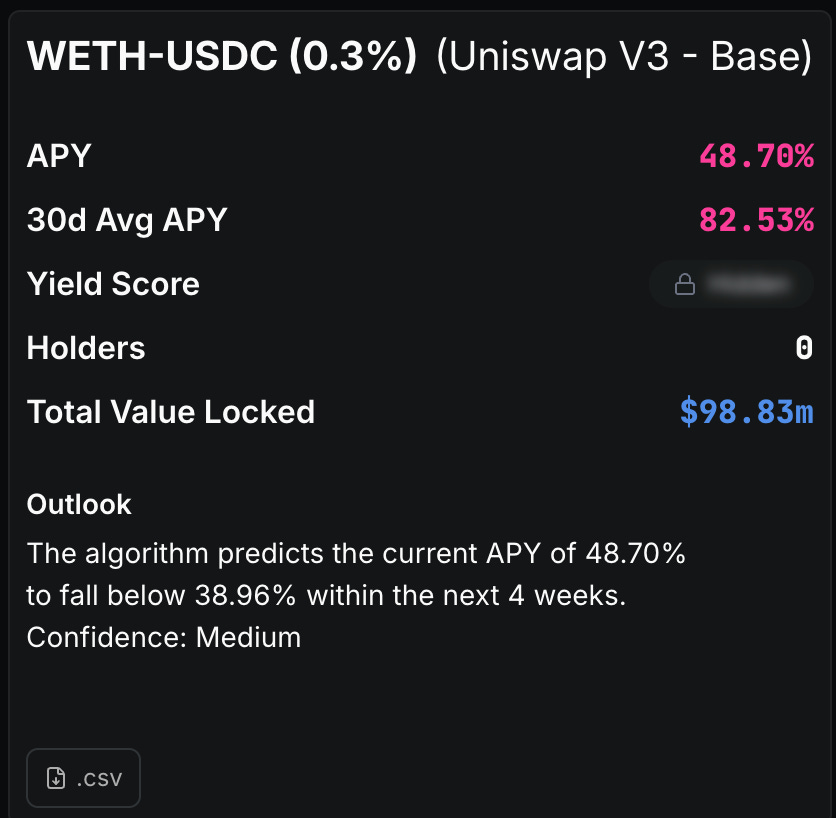

2. Uniswap V3 WETH/USDC

The cleaner comparison is Uniswap V3.

The WETH/USDC pool on Base is showing roughly 48.70% APY in the current snapshot, and the important part is that this is fee-driven. No AERO rewards. No gauge voting. No token emissions trying to make the number look better.

That makes it one of the stronger signals in the whole issue.

A high fee APY on a deep WETH/USDC pool means traders are actually using Base. That is harder to fake than TVL. Capital can be incentivized. Volume and fees have to keep showing up.

The risk is still concentrated liquidity. You are not just “earning 48.70%.” You are underwriting a WETH/USDC range. If ETH moves outside your range or volatility picks up, the pool can become much less comfortable very quickly.

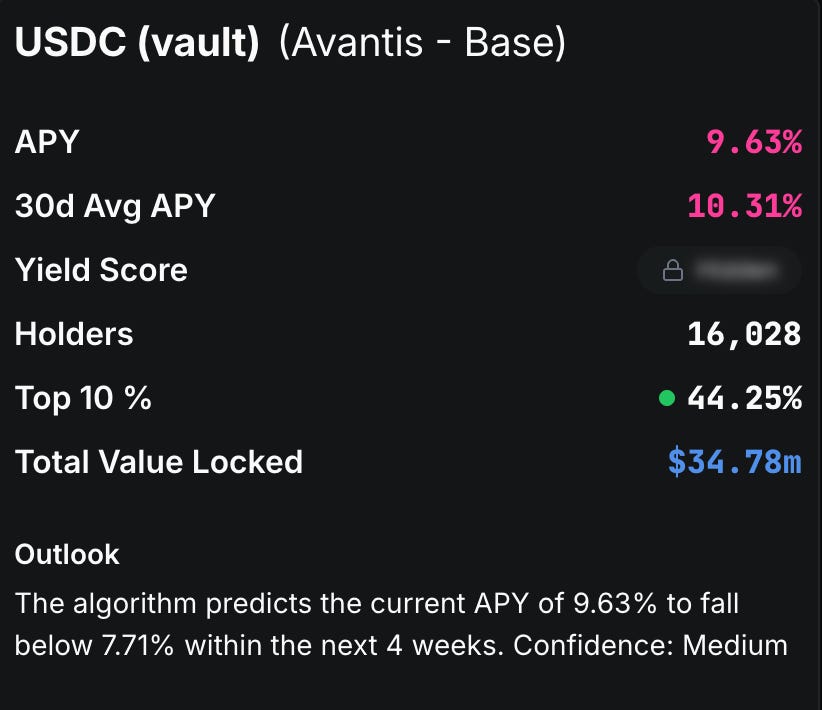

3. Avantis USDC LP

Avantis is the more interesting passive option.

Instead of managing a DEX range, you deposit USDC as counterparty liquidity for perp traders. The current snapshot shows roughly 10% APY with about $35M in protocol TVL.

The appeal is obvious: single-sided USDC, no impermanent loss, no range management.

The risk is also different. You are taking exposure to perp trader flow and protocol design. Perp DEXs are more complex than simple lending markets. Funding, trader PnL, liquidations, oracle assumptions, and contract risk all matter.

So I would not put Avantis in the same “safe stablecoin yield” bucket as lending. It is more like structured market-making exposure with a simpler user interface.

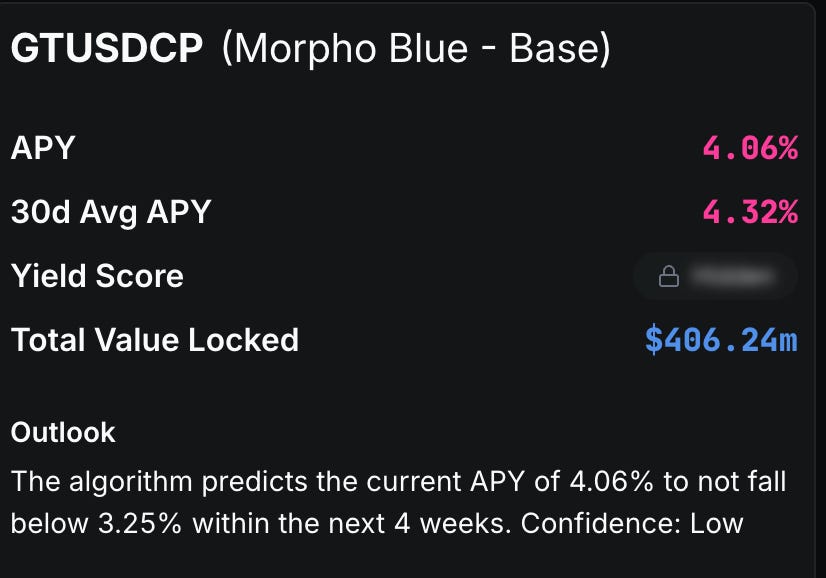

4. Morpho Blue USDC

Morpho is the most straightforward lending option on Base.

The USDC market snapshot is around 4.06% APY. Nothing dramatic. But that is partly the point.

The yield comes from borrowers paying variable interest. No LP range. No perp counterparty exposure. No need to care about AERO emissions or trading volume every day.

For a reader who wants Base exposure without turning every deposit into an active strategy, this is probably the first place to look.

The risk is lower, not zero. Lending markets still depend on collateral quality, oracle behavior, utilization, liquidation mechanics, and vault curation. Morpho is a strong protocol, but the exact market matters more than the logo.

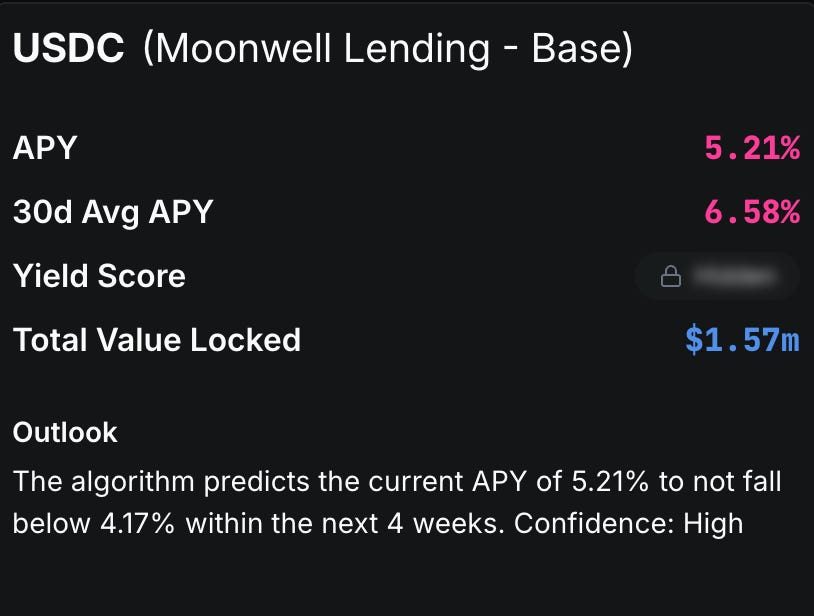

5. Moonwell USDC

Moonwell is the smaller lending option.

Its USDC market is showing roughly 5.21% APY, split between lending interest and WELL incentives. The TVL is much smaller than the largest Morpho or Aave-style markets, which cuts both ways.

Smaller pools can sometimes pay a better rate because utilization moves faster. They can also become unstable faster when one large depositor or borrower changes the balance.

I would treat Moonwell as a Base-native lending bet, not the default stablecoin parking place. The rate is fine, but the market depth matters.

How I Would Think About It

The high headline APYs are in DEX liquidity. Aerodrome and Uniswap can pay well because Base has real trading activity, but they require active management and IL risk.

The more boring yields are in USDC lending. Morpho and Moonwell are easier to understand, easier to monitor, and much less likely to surprise you with range problems.

Avantis sits in the middle. It gives you single-sided USDC, but the risk comes from perp market structure instead of lending utilization.

The strongest signal this week is not that Base has one amazing pool. It is that Base now has a full yield curve: active LP, fee-only LP, perp LP, lending, and incentive-backed lending.

That is what mature DeFi chains start to look like.

Base does not need a token for this to matter. In some ways, the lack of a token makes the signal cleaner. There is no native asset distorting the read. The question is just whether capital, volume, and useful protocols keep showing up.

Right now, they are.

🧐 Onchain Analytics

This is what I have actually been watching onchain this week.

Lending Is Recovering, But Not Everywhere

The lending market looks calmer than it did two weeks ago.

During the sell-off, Aave was printing $6.4M/day in liquidation fees and Morpho fees were up 372%. That was not normal growth. That was leverage getting forced out of the system.

Now the numbers look more balanced. Aave V3 is at $11.8B TVL, up 4.3% this week. Morpho Blue is at $6.67B, up 5.5%. SparkLend is at $3.34B, up 8.3%.

Fees are cooling too. Total DeFi fees over the past 7 days were $371M, down from $430M in the prior 7-day period. That is what you want to see after a stress event. The system worked, the fee spike faded, and capital started moving again.

The split is the part I care about. SparkLend is growing faster than Aave and Morpho. Maple bounced 13% to $2.12B. Kamino Lend on Solana went the other way, down 15.6% to $1.08B.

So lending is recovering, but not evenly. Capital is moving back toward Ethereum-aligned and institutional credit markets first. Solana lending is not getting the same bid this week.

The caveat is Maple. A 13% weekly bounce looks good, but one week does not prove a credit cycle has turned. I would want to see that TVL hold through another volatile week before treating it as a real trend.

RWA Is Starting To Sort Winners From Experiments

RWA TVL is roughly flat at $25.9B, but the category is not standing still.

Centrifuge is up 18.1% to $1.63B. Circle USYC is at $3.01B, up 6.5%. OpenEden TBILL is up 28.3% to $216M. BUIDL keeps grinding higher at $3.03B, up 2.6%.

At the same time, Ethena USDtb is down 9.2% to $916M and WisdomTree dropped 9.6%.

That is the useful signal. RWA is no longer just one broad trade where everything moves together. Capital is starting to separate the deeper, more institutionally credible products from the smaller experiments.

For anyone allocating to RWA products, APY is not enough. The better questions are: who is the issuer, how deep is the liquidity, who holds the token, and how clean is the redemption path?

The caveat is Centrifuge. An 18% weekly move is strong, but it could still be one large allocation. The real test is whether the capital stays over the next 30 to 60 days.

Base Is Quiet, Which Is Fine

Base did not have a dramatic week. That is not a bad thing.

Base bridge TVL is at $2.37B, up 3.8% weekly. Arbitrum is at $2.72B, up 3%. After the recent volatility, modest growth across both chains is healthier than another zero-sum rotation.

The number I keep coming back to is Base stablecoin supply: $4.76B, according to DefiLlama. That is a lot of capital sitting on the chain before it shows up in lending, DEX volume, or yield vaults.

Aerodrome still dominates the Base DEX story, but the stablecoin base matters more for the next leg. If confidence improves, Base already has the dry powder for lending markets, LP positions, and yield products to grow without needing a new bridge wave first.

The caveat is that stablecoin supply is not the same as deployable DeFi capital. Some of it sits in Coinbase-linked wallets, CEX flows, or passive balances that may never touch a protocol. Still, the raw base is there.

📚 This Week’s Intel

A few stories worth your time that did not make the main thesis.

1. Japan’s Lower House Passes Sweeping Crypto Bill — 20% Flat Tax Rate

Japan’s legislature passed a bill amending the Financial Instruments and Exchange Act to regulate cryptocurrencies more like securities. The standout change: a flat 20% tax rate on crypto gains, down from up to 55% for high earners. The bill also creates a clear regulatory path for crypto ETFs.

This matters because Japan is not a small market. 127 million people, one of the world’s deepest capital markets, and a government that has been methodically building crypto infrastructure for years. If the upper house clears it, this could become one of the more important regulatory shifts of the year.

The caveat: Japan has had progressive crypto laws before, and adoption has not always followed. Tax cuts help, but they do not automatically create demand.

Source: Unchained Crypto

2. BlackRock Files Final Amendment for BITA — a Yield-Bearing Bitcoin ETF

BlackRock submitted what appears to be the final filing for BITA, a covered-call Bitcoin ETF. The fee: 65bps, cheaper than many actively managed crypto products. The mechanism: BlackRock sells Bitcoin call options, collects the premium, and pays it out as yield to holders.

Why it matters: this gives income-focused investors a regulated way to get BTC exposure with cash flow, which is a different thesis than spot BTC alone.

The risk: covered-call strategies cap upside. In a bull market, you collect yield while missing part of the move. In a flat or slightly up market, they can work well. Know what you are buying.

Source: Unchained Crypto

3. CFTC Proposes First Formal Rulemaking for Prediction Markets

The CFTC released a 90-day framework to vet event contracts covering areas like war, gaming, assassination, and terrorism. This is the agency’s first formal rulemaking for prediction markets after years of ad-hoc enforcement actions.

The downstream impact is direct: Polymarket, Kalshi, and Hyperliquid’s new prediction-market expansion all operate in the regulatory gap this rule would narrow. A clear framework is better than the current uncertainty, but the scope of prohibited contracts will decide how much room the category has in the US.

The outcome matters for DeFi because prediction markets are one of the few crypto categories generating real, repeatable fees outside of perps and lending. A restrictive rule could cap that growth.

Source: Unchained Crypto

4. Tether Backs Neura’s Robotics Round

Tether participated in Neura’s large robotics funding round, reportedly worth up to $1.4B. The broader idea is to connect Tether’s wallet and edge-computing work with robots and machine-to-machine payments.

This fits Tether’s machine economy thesis. The company has been moving beyond stablecoins into mining, AI infrastructure, education, and now robotics.

The caveat: this is years out. Robots need to ship, customers need to care, and Tether’s non-stablecoin bets still carry execution risk.

Source: FT / WSJ coverage, plus Unchained Crypto

5. Centrifuge TVL Surges 18% to $1.63B

Centrifuge, the RWA credit marketplace, added roughly $250M in TVL this week, an 18% move to $1.63B. For context, most DeFi lending protocols are flat or recovering, while Centrifuge is growing.

Why it matters: Centrifuge is one of the cleaner institutional credit stories in DeFi. It connects real-world borrowers with onchain liquidity. The growth suggests institutional credit demand is real, not just a narrative trade.

The caveat: $250M in one week could be one large allocation from a single investor. The real test is whether the TVL holds over the next 30 to 60 days. Watch fee generation, not just the headline number.

🎧 Podcast Picks

Podcasts worth your time this week.

The Rollup: DeFi Dad: The Ethereum Bull Thesis In 2026

This one fits the Base issue because Base is still an Ethereum-aligned bet. DeFi Dad talks through ETH staking yield, RWA tokenization, and why Ethereum’s role as settlement layer still matters even when attention moves to faster venues.

The useful part is not the ETH bull case by itself. It is the framing: if ETH becomes the base collateral and settlement layer for onchain finance, chains like Base become part of that distribution layer.

Empire: CFTC Chair Michael Selig On Perps, Prediction Markets & Crypto In The U.S

Worth listening to after the CFTC item above. The discussion covers US perps, prediction markets, DeFi regulation, 24/7 markets, and coordination with the SEC.

For DeFi readers, this matters because perps and prediction markets are two of the few crypto categories with real fee demand. The open question is how much of that activity can survive inside a US regulatory framework.

That’s it for this week.

If you found this useful, share it with someone who is trying to make sense of this market.

You can also follow me on X and Farcaster for more frequent updates.

Nothing in this newsletter is financial advice.

I personally use many of the protocols I write about, but that does not make them safe. Crypto is risky, DeFi is risky, and things can break quickly.

Do your own research, size positions carefully, and never invest more than you can afford to lose.